Conducting horizontal and vertical balance analysis. Vertical analysis

Hi, Vasily Zhdanov is in touch in this article, we will consider the horizontal and vertical analysis of the company's balance sheet. Accounting is the most important aspect of a serious business organization. But the ability to analyze the balance sheet is also important, because the data recorded in it can tell the expert about the past and current activities of the company, as well as predict the development of the company in the future. Depending on how much information the analyst needs, and what specific goals he pursues, one of the many existing methods of balance analysis is selected. But the most popular are horizontal and vertical balance analysis, because both methods allow:

- reduce the risks of creditors when investing in a company;

- develop methods to maintain the stability of production;

- increase the income of the company;

- conduct a competent analysis of financial statements.

Important! Horizontal and vertical balance sheet analysis can be applied at the same time, since they complement each other and help conduct a deeper study of accounting data, which allows you to see the company's growth rates and dynamics of its development.

Summary of the balance sheet

The balance sheet is a key type of reporting, thanks to which the management staff at the company has the opportunity to see the dynamics of the enterprise's development in specific figures, the presence of short-term and long-term debts, the origin of funds, as well as the amount of fixed / working capital.

The balance sheet is often called the financial entity, due to the fact that the information contained in the reporting clearly demonstrates to the managers of the company and analysts the risks of ruin and development prospects, as well as the rate of growth (recession).

The balance sheet results in 2 parts, equal to each other (if the balance is drawn up correctly):

- ASSETS(money, material values, machinery, equipment, buildings and structures, stocks, debts of counterparties and consumers, etc.) - everything that the company owns and disposes for the purpose of carrying out commercial activities and making a profit.

- LIABILITIES(short-term liabilities to counterparties and customers, borrowed funds, retained earnings, equity (share) capital) - information about the sources of the firm's assets.

Horizontal and vertical analysis of the business can help the management of companies in finding weaknesses in the company's activities and options for correcting errors.

Horizontal balance analysis. Example with conclusions

The method of analysis that will be discussed is called horizontal for the reason that information on each item of the balance sheet for several periods is located horizontally in a line. The more activity periods the data is compared, the more columns in the analysis table.

Below is a list of basic information that you need to know about the horizontal analysis of financial statements:

- This method is used in cases where a study of the temporal dynamics of the balance sheet totals is required.

- Not only the values of absolute indicators (in rubles), but also of relative ones (in%) are subject to comparison:

| Absolute deviations |  |

| Relative deviations |  |

| Rates of growth |

- To conduct the analysis, you should select 2-3 quarters or years. Absolute (or relative) values are sequentially compared with similar indicators of later periods.

- Horizontal analysis makes it possible to assess whether the production performance has improved or deteriorated in comparison with the year before last and last year.

When conducting horizontal analysis, first of all, they look at the balance sheet total for the Asset - if the value increases in columns (from previous to future periods), this indicates a favorable development of the company and that it has chances for further growth.

Further, attention is drawn to the dynamics of indicators of non- and circulating assets: if their growth is observed from period to period, it means that the company is actively working, and the management personnel makes the right decisions on the way to improving the base.

The next thing to check is the company's solvency, whether the company has free money in circulation and, which is important, whether it is used for investments in order to extract additional funds. arrived. All this can be judged by examining the dynamics of values for items directly related to money - "Cash", "Accounts receivable", "Financial investments".

Finally, passive strings are examined. To understand where the company under study has free money, you should pay attention to the changes in the indicators under the items "Borrowed funds" and "Accounts payable". Here, before drawing any conclusions, you need to carefully analyze the company's policy in terms of attracting third-party capital. Since the analysis of the balance sheet may show an increase in debt, however, this can be a positive point if the money is correctly invested and brings additional income.

Vertical balance sheet analysis (structural). Examples with conclusions

Basic information about vertical analysis of accounting data can be seen in the list below:

- Structural analysis is to demonstrate the structure of the final account information. reporting in the form of relative indicators, expressed as a percentage. As a result of the research, the expert receives the values of all balance sheet items in% to its total.

- The advantage of vertical analysis over horizontal analysis is that it is difficult to see in absolute terms whether there is a positive or negative trend in the company's work. Relative values, on the contrary, make it easy to assess whether financial indicators have deviated for the better or worse, and to what extent. The resulting output data in relative terms will not allow making incorrect comparisons due to the influence of various external factors, such as the inflationary process.

- This method of analysis differs from horizontal analysis in that vertical analysis is focused on a selected moment and gives an assessment of the position of the company on the day the report is drawn up. The method is used when necessary:

- to see how, in comparison with previous periods, certain articles of the bukh have changed. balance;

- compare the capital structures of several firms or enterprises of different fields of activity;

- find out the composition of non- and working capital;

- find out whether the amount of the company's borrowed capital has decreased or increased;

- check how the structure of liabilities and assets has changed.

The essence of using structural balance sheet analysis is as follows:

- The total amount of proceeds when analyzing the statement of financial results of the company (form No. 2) is taken equal to 100%. If the balance sheet is examined, the total amount of assets is taken as 100%. Vertical analysis is also suitable for examining the statement of cash flows (form No. 4) and changes in equity (form No. 3).

- All balance sheet items separately are calculated as a percentage of 100% (that is, of the total amount of assets or revenue). To implement this, the analyst must select the period (year) of the analyzed firm, and then divide each line of the balance sheet separately by the currency Bukh. balance, and then multiply the result by one hundred percent (since the value should be relative, in%).

Let's return to step 2 of the algorithm, which was given above the table. Let's find out how the values in the table were obtained using the example of current assets:

Now that we understand how the data in the table was calculated, let's analyze it and draw conclusions:

- The size of the long-term debt of the analyzed company decreased slightly.

- The amount of equity (equity) capital is 50% of the total liability (this indicates that the company is characterized by an average level of stability).

- Short-term debt makes up a third of the balance sheet and remains practically unchanged.

- The number of OS objects decreases because some of them are out of circulation.

- 63% of assets account for working capital, and the increase in their share was a consequence of the growth of accounts receivable (the company's management should think about the reasons for its growth).

Let's try to conduct a vertical analysis of data for 2 years of operation of the enterprise in absolute and relative terms:

In general, professional financial analysts and auditors are involved in the interpretation of a set of balance sheet outputs, since it is necessary to be able to see the big picture and draw conclusions based on a comprehensive study. What can be said unequivocally to a layman, looking at the table we received, is that:

- the analyzed company does not change the indicator of equity capital in the form of authorized capital, but the amount of available equity capital increased by 8% due to the presence of retained earnings;

- the company has attracted a fairly large amount of borrowed funds, the Liability includes> 60% of accounts payable, but the positive side is the decrease in the level of loans in dynamics;

- the company is solvent and fairly stable financially, since there is a decent level of cash (48.22%);

- the company illiterately chooses counterparties for cooperation, most likely the current partners are insolvent, because there is a high level of accounts receivable;

- the data from the table indicate that the level of receivables and stocks of the company is high, and therefore there are fewer non-current assets than current assets (the bad thing is that there may be unnecessary costs for storing stocks (logistics), but the good thing is that managers take care of investing into uninterrupted production).

Answers to frequently asked questions on "Horizontal and vertical balance analysis"

Question: What are the advantages and disadvantages of using vertical and horizontal analysis of financial statements?

Answer: The positive side of horizontal analysis is the ability to assess the dynamics of financial indicators over the years. A significant drawback is the fact that this type of analysis is not very suitable for assessing the financial condition and decision-making by managers - it is rather a diagnostic method. With regard to vertical analysis, it makes it possible to track changes in the structure of A and P of the firm, but also does not allow assessing its financial condition.

Balance analysis is carried out using one of the following methods:

- ? analysis directly on the balance sheet without preliminary changes in the composition of balance sheet items;

- ? by constructing a condensed comparative balance sheet with the aggregation of some elements of the same composition of balance sheet items;

- ? additional adjustment of the balance sheet for the inflation index, followed by the aggregation of items in the necessary economic sections. Comparative analytical balance can be obtained from the initial balance by compaction of individual items and supplementing it with indicators of structure, dynamics and structural dynamics.

Analytical balance is useful in that it brings together and systematizes the calculations that the analyst usually performs when familiarizing with the balance sheet. The analytical balance sheet usually covers a lot of important indicators that characterize the statics and dynamics of the financial condition of the organization. This balance actually includes indicators of both horizontal and vertical analysis. Directly from the analytical balance, you can get a number of the most important characteristics of the financial condition of the organization. These include:

the total value of the organization's property, reflected in the final line of the balance sheet;

the cost of immobilized (non-current) assets, equal to the total of section I of the balance sheet;

the cost of mobile (circulating) funds, equal to the total of section II of the balance sheet;

the cost of material circulating assets (stocks);

the amount of the organization's own funds, equal to the total of section III of the balance sheet;

the amount of borrowed funds, equal to the sum of the results of sections IV and V of the balance;

the amount of own circulating assets, equal to the difference in the results of sections III and I of the balance;

A separate item of the aggregate balance sheet shows the net working capital, defined as a part of the current assets (working capital), financed from the invested capital. The value of this indicator characterizes the degree of liquidity of the enterprise, which makes this indicator of particular importance.

Typically, net working capital (PER) is calculated using the formula

CHOK = TA - TP,

where TA is current (circulating) assets,

TP - current (short-term) liabilities.

The greater the value of the net working capital, the more financially stable the enterprise.

Analyzing the comparative balance sheet, it is necessary to pay attention to the change in the proportion of the value of own working capital in the value of the property, to the ratio of the growth rates of equity and borrowed capital, as well as to the ratio of the growth rates of receivables and payables.

With stable financial stability, the organization should increase in dynamics the share of its own working capital, the growth rate of equity capital should be higher than the growth rate of borrowed capital, and the growth rate of receivables and payables should balance each other.

Horizontal balance analysis consists in the construction of one or more analytical tables, in which the absolute balance sheet indicators are supplemented by indicators of dynamics. The degree of aggregation of indicators is determined by the analyst.

Table 1 - Horizontal analysis of the balance sheet asset

|

Asset Articles |

At the beginning of the year, thousand rubles |

At the end of the year, thousand rubles |

Changes (+, -) |

|

|

in thousand rubles |

||||

|

Fixed assets- total, including: |

||||

|

Intangible assets |

||||

|

Fixed assets |

||||

|

Construction in progress |

||||

|

Deferred tax assets |

||||

|

Other noncurrent assets |

||||

|

Current assets- total, including |

||||

|

Cash |

||||

|

Other current assets |

||||

|

Total assets |

Based on the above table. 1. we can conclude the following. The total value of the organization's property increased over the reporting year by 33,538 thousand rubles, or 140.65%.

The most significant increase in absolute terms was the least mobile part of current assets - inventories, and in relative terms - cash. There is a fairly significant increase in accounts receivable (see Appendix 1). This fact reflects the diversion of part of current assets to lending to consumers of finished products, goods, works and services of the organization, subsidiaries and other debtors, which indicates the actual immobilization of this part of the working capital from the production process. On the other hand, accounts receivable indicate the forthcoming receipt of funds, if the organization has solvent debtors.

Non-current assets for the reporting period increased by 24455 thousand. RUB, or 140.68%. The growth in the value of non-current assets occurred due to an increase in the value of fixed assets and the formation of deferred tax assets, as well as under the item "Construction in progress"

Table 2 - Horizontal analysis of balance sheet liabilities

|

Liabilities Articles |

At the beginning of the year, thousand rubles |

At the end of the year, thousand rubles |

Changes (+, -) |

|

|

in thousand rubles |

||||

|

Capital and reserves- total, including: |

||||

|

Authorized capital |

||||

|

Extra capital |

||||

|

Reserve capital |

||||

|

long term duties- total, including |

||||

|

Loans and credits |

||||

|

short-term obligations- total, including |

||||

|

Loans and credits |

||||

|

Accounts payable |

||||

|

revenue of the future periods |

||||

|

Provisions for future expenses |

||||

|

Total liabilities |

As follows from the calculations presented in table. 2., an increase in the value of liabilities for the reporting period by 33,538 thousand rubles, or 140.65%, is mainly due to an increase in own funds by 14,176 thousand rubles, or 121.44%. Long-term liabilities for the same period increased by 15,000 thousand rubles, and short-term - by 4,362 thousand rubles. (126.59%).

The growth of own funds was due to the growth of retained earnings in the amount of 14,176 thousand rubles. The authorized, additional and reserve capital did not change in absolute amounts.

In the structure of borrowed funds, the most significant increase was the debt to participants in the payment of income - by 2,694 thousand rubles.

The next analytical procedure is vertical analysis - presentation of the financial statement in the form of relative indicators. Such a presentation allows you to see the share of each balance sheet item in its overall total. An obligatory element of the analysis is the time series of these values, by means of which it is possible to track and predict structural changes in the composition of assets and sources of their coverage. Thus, two main features of vertical analysis can be distinguished:

the transition to relative indicators allows for a comparative analysis of enterprises, taking into account industry specifics and other characteristics;

relative indicators smooth out the negative impact of inflationary processes, which significantly distort the absolute indicators of financial statements and thus make it difficult to compare them in dynamics.

It should be noted that the importance of permanent and current assets for manufacturing and trading companies is different. Thus, a significant part of the assets of a production company will obviously be formed at the expense of fixed assets. At the same time, the assets of a trading firm will mainly consist of inventories, goods for resale and other property, which is reflected in the section “Current assets”. Thus, when analyzing the ratio of permanent and current assets, more attention should be paid to the change in the structure itself, and if possible, compare it with the structure of assets of analogous companies and find out the reasons for the differences.

Table 3 - Vertical analysis of the balance sheet asset

|

Asset Articles |

Share at the end of the year,% |

Change in structure (+ -) |

|

|

Fixed assets- total, including: |

|||

|

Intangible assets |

|||

|

Fixed assets |

|||

|

Construction in progress |

|||

|

Profitable investments in material assets |

|||

|

Long-term financial investments |

|||

|

Deferred tax assets |

|||

|

Other noncurrent assets |

|||

|

Current assets- total, including |

|||

|

VAT on purchased assets |

|||

|

Long-term receivables |

|||

|

Short-term receivables |

|||

|

Short-term financial investments |

|||

|

Cash |

|||

|

Other current assets |

|||

|

Total assets |

Both at the beginning and at the end of the reporting period, non-current assets occupy a larger share in the property than current assets. During the reporting year, their share increased by 0.02 points, which indicates the formation of a more stable structure of assets.

Table 4 - Vertical analysis of the balance sheet liability

|

Liabilities Articles |

Share at the beginning of the year,% |

Share at the end of the year,% |

Change in structure (+ -) |

|

Capital and reserves- total, including: |

|||

|

Authorized capital |

|||

|

Own shares repurchased from shareholders |

|||

|

Extra capital |

|||

|

Reserve capital |

|||

|

Retained earnings (uncovered loss) |

|||

|

long term duties-total, including |

|||

|

Loans and credits |

|||

|

Deferred tax liabilities |

|||

|

Other long-term liabilities |

|||

|

short-term obligations-total, including |

|||

|

Loans and credits |

|||

|

Accounts payable |

|||

|

Indebtedness to participants for payment of income |

|||

|

revenue of the future periods |

|||

|

Provisions for future expenses |

|||

|

Other current liabilities |

|||

|

Total liabilities |

From table. 4. it can be seen that equity capital prevails in the structure of the organization's liabilities. By the end of the year, there was a tendency towards a slight decrease in its share.

In the process of analysis, special attention should be paid to the elements that have the highest specific gravity, and the elements, the proportion of which changed abruptly. As a rule, elements with the maximum specific weight or changing in leaps and bounds are indicators of "problem points" of the organization. To obtain more accurate information, it is necessary to estimate the absolute values of these elements.

Based on the results of the analysis of the balance sheet as a whole, we can conclude the following. The analysis of the indicators of structural dynamics revealed the presence of a rather favorable trend: the increase in property was provided due to the increase in non-current assets. Thus, the newly attracted financial resources were invested mainly in liquid assets, which enhances the financial stability of the organization. The greatest influence on the increase in the sources of funds was made by the increase in equity capital.

Horizontal and vertical analysis complement each other. Therefore, in practice, it is advisable to build analytical tables that characterize both the structure of the accounting form and the dynamics of its individual indicators.

Trend analysis - part of the forward-looking analysis that is necessary in the management of the financial resources of the organization. In the process of trend analysis, a graph of the possible development of the organization is built, the average annual growth rate is determined and the predicted value of each indicator is calculated. This is the easiest way to make financial forecasting. The elimination of random deviations allows us to identify stable time series of individual indicators, which can serve as a fairly reliable basis for predicting the development of economic entities.

Analysis of the dynamics of the balance sheet currency, the structure of assets and liabilities of the organization allows us to draw a number of important conclusions necessary both for the implementation of current financial and economic activities, and for making managerial decisions for the future.

In general terms, the hallmarks of a “good” balance are:

balance sheet currency at the end of the reporting period increased compared to the beginning;

the growth rate of current assets is higher than the growth rate of non-current assets;

the organization's own capital exceeds the borrowed capital and its growth rate is higher than the growth rate of borrowed capital;

the growth rates of receivables and payables are approximately the same.

The analysis of the financial and economic condition of the enterprise is carried out using a set of methods and working techniques (methodology) that allow you to structure and identify the relationship between the main indicators.

Financial statements consist mainly of quantitative, absolute indicators. Therefore, the analysis of certain indicators, economic phenomena, economic processes, situations begins with the consideration of absolute values in natural or value terms. These indicators are basic in financial accounting. In analysis, they are used to calculate averages and relative values. For the analysis of absolute indicators is used. As a rule, a comparison method, with the help of which the absolute or relative changes in indicators, trends and patterns of their development are studied.

The analysis of absolute indicators is the study of the data presented in the financial statements: the composition of the property of the enterprise, the structure of financial investments, sources of formation of equity capital is determined, the amount of borrowed funds is estimated.

The balance sheet serves as an indicator for assessing the financial condition of the company.

The purpose of a horizontal balance sheet analysis is to visualize the changes that have occurred in key balance sheet items and to help company managers make decisions about how to proceed.

Horizontal analysis consists in comparing the financial data of the enterprise for the past two years in relative and absolute form in order to identify trends in changes in balance sheet items or their groups and, on the basis of this, calculate the basic growth rates.

The analysis technique is quite simple: sequentially in the second and third columns, data on the main balance sheet items at the end and at the beginning of the year are placed. Then, in the fourth column, the absolute deviation of the value of each balance sheet item is calculated. The last column gives the relative change in percentage of each item.

Analysis of the property status of an economic entity includes an assessment of the value of its assets, their dynamics. The analysis is carried out on the basis of the information contained in the asset of the balance sheet of the organization. Assets are understood as property (resources of an enterprise) in which money is invested.

Current assets are more liquid than non-current assets. This is due to the fact that non-current assets constitute that part of the property of the enterprise that is not intended for sale, but is constantly used for the production, storage and transportation of products. Current assets participate in a constant cycle of converting them into cash. Current assets can also be divided according to the degree of liquidity: the most liquid assets are cash, securities, then, according to the degree of diminishing liquidity, there are accounts receivable, reserves and costs.

A horizontal analysis is carried out for all the indicated sections, i.e. the indicators for a number of analyzed periods are compared, the dynamics of indicators is monitored.

Consider the horizontal analysis of the asset balance of Mars-Plus LLC for 2006, 2007, 2008. (Appendix A, B) performed in table 2.1

Table 2.1 - Horizontal analysis of the balance sheet asset of Mars-Plus LLC

|

The balance of the enterprise on |

Change 2007 to 2006 |

Change 2008 to 2006 |

|||||

|

Absolute thousand rubles |

Relative% |

Absolute thousand rubles |

Relative% |

||||

|

Fixed assets |

|||||||

|

Fixed assets |

|||||||

|

Deferred tax assets |

|||||||

|

Current assets |

|||||||

|

Raw materials, materials |

|||||||

|

Finished products |

|||||||

|

Accounts receivable |

|||||||

|

Cash |

|||||||

|

Assets, total |

Based on the data in Table 2.1, the following conclusions can be drawn: in 2007 compared to 2006, there was a decrease in the total value of the company's property by more than 25%. Current assets decreased over the period to a greater extent than non-current assets. The cost of fixed assets decreased by more than 17%, this was caused by the write-off of depreciation and the fact that in 2007 the company practically did not invest in the acquisition of fixed assets. The most significant decrease in relative terms was in the balances of finished goods - by 86.2%. This negatively affected the financial condition of the organization, as the decline occurred not only due to the acceleration of implementation, but also due to a sharp decrease (by more than 20%) in the catch. A significant decrease in the cost of inventories (more than 20%) was caused by the impossibility of their replenishment, since the enterprise was experiencing financial difficulties due to a decrease in catch and fishing in the Bering Sea, which resulted in a significant increase in production costs and the release of new, uncompetitive products.

There is a decrease in accounts receivable, which is a positive factor, since the volume of sales decreased by 22%, and debt by 28%, therefore, the state of settlements with customers has improved. Cash growth by 67% indicates that the value of the quick liquidity ratio has improved, but given the financial difficulties that the company experienced in 2007, it should not have frozen funds in current accounts.

In 2008, compared to 2006, the volume of the company's resources decreased by 34%. Non-current assets decreased to a greater extent than current assets. The cost of fixed assets decreased by 32%, which indicates that the company did not purchase fixed assets. The most significant, by 91.5%, decreased the balance of finished products, this indicates the acceleration of sales, which confirms the increase in catch by more than 40%. Considering that the excessive diversion of funds to work in progress and finished products leads to the death of resources and inefficient use of working capital, a decrease in this indicator has a positive effect on the financial condition of the company. There was a slight decrease in inventories as a result of the repairs carried out and the write-off of spare parts. In connection with a significant increase in sales, there is an increase in accounts receivable - by 35%. This fact reflects the diversion of part of current assets to lending to consumers of finished products, which indicates the actual immobilization of this part of working capital from the production process. On the other hand, given that the receivables are not overdue and the company has solvent debtors, the debt indicates an impending cash flow. There has been a significant increase in cash. They were formed due to significant receipts of funds from product buyers in the last week of the year. Considering the fact that the organization has large debts to suppliers, freezing funds in current accounts does not seem to be effective.

The liability of the balance sheet reflects the sources of financing of the enterprise's funds, grouped at a certain date according to their ownership and purpose. Liabilities to owners constitute an almost constant part of the balance sheet liability that is not subject to repayment during the activities of the organization. Liabilities to third parties have different repayment periods: less than one year - short-term, more than one year - long-term.

In table 2.2, consider a horizontal analysis of the balance sheet liabilities for 2006, 2007 and 2008.

horizontal vertical analysis balance

Table 2.2 - Horizontal analysis of the liabilities of the balance sheet of Mars-Plus LLC

|

The balance of the enterprise on |

Change 2007 to 2006 |

Change 2008 to 2006 |

|||||

|

Absolute thousand rubles |

Relative% |

Absolute thousand rubles |

Relative% |

||||

|

Capital and reserves |

|||||||

|

Authorized capital |

|||||||

|

Undestributed profits |

|||||||

|

Short-term liabilities |

|||||||

|

Loans and credits |

|||||||

|

Accounts payable, incl. |

|||||||

|

Supplier and contractors |

|||||||

|

Debts to staff |

|||||||

|

Debts to extrabudgetary funds |

|||||||

|

Tax arrears |

|||||||

|

Liabilities, total |

As follows from the calculations presented in Table 2.2, in 2007 compared to 2006, the following changes took place: the decrease in the value of liabilities was caused by a decrease in short-term liabilities by 29%. A significant increase in equity was due to an increase in retained earnings by 97%. The authorized capital has not changed. The company does not attract long-term borrowed funds, i.e. there is no investment in production. Borrowed funds have tripled, which indicates that the company does not have enough own funds to settle its obligations. In the structure of accounts payable, there was a 34% decrease in debt to suppliers and contractors, an increase in debt to personnel by 65% due to an increase in wages and the accrual of bonuses in December based on the results of the year. Debts to extra-budgetary funds and the budget increased by 16% and 31%, respectively, but it is current and was repaid on time.

In 2008, compared to 2006, the profit of the enterprise doubled, which was influenced by a significant increase in revenue (by 40%), while the cost of production increased by only 26%. The company attracted 2 times more borrowed funds, which were used to replenish inventories. As part of accounts payable, there was a decrease in debt to suppliers and contractors. Considering that the company purchases the main supplies outside the Russian Federation, due to the fall in the dollar exchange rate, the debt to suppliers decreases. The payroll debt to the personnel increased, which was caused by the increase in wages. As a result, there is an increase in debt to extra-budgetary funds and tax authorities. All debts are current and are paid off on time.

Vertical analysis Is a method for diagnosing the financial condition of an organization and assessing the dynamics of changes in the structure. The purpose and essence of vertical analysis of financial statements is to analyze changes in the structure of financial indicators for the period under review. This analysis is used to assess the structure of the balance sheet, income statement and cash flow statement. In the article, we will consider how the vertical analysis of the balance sheet and the statement of financial results is carried out using the example of the enterprise PJSC "KAMAZ".

The directions of the vertical analysis of the organization's balance sheet are as follows:

- Assessment of structural changes in the company's assets / liabilities.

- Calculation of the change in the share of the organization's borrowed capital.

- Determination of the composition of circulating and non-circulating capital.

- Comparison of the capital structure of different companies or companies in different industries.

Vertical analysis can be applied not only to the balance sheet, but also to the statement of financial results ( form number 2) when determining the structure of income and expenses. For example, to diagnose the structure of revenue or profit from sales, etc. Vertical analysis can similarly be used for the statement of changes in equity ( form No. 3) and the statement of cash flows ( form No. 4), but, as a rule, vertical analysis is limited to the balance sheet and income statement.

Comparison of vertical balance sheet analysis with other methods of financial analysis

Vertical analysis is one of the tools (methods) for analyzing the financial statements of an organization for diagnosing a negative trend in indicators, a decrease in financial stability due to an increase in the share of borrowed capital, etc. In addition to it, other methods are also used ⇓.

| Financial Statement Analysis Title | Directions of application | Advantages | Flaws |

| Vertical analysis (analogue: structural analysis) |

It is used to determine the capital structure of the organization, financial indicators and the change in the structure over time | Allows you to track structural changes in the assets and liabilities of the company | Used for diagnostics Does not assess the financial condition of the enterprise |

| Horizontal analysis (analogue: trend analysis) |

Used to assess the direction and predict the dynamics of changes in financial indicators | Allows you to assess the dynamics of changes by years of financial indicators | Serves more for diagnostics, and not for making management decisions and assessing the financial condition |

| Coefficient analysis | Assessment of financial indicators characterizing: profitability, financial stability, turnover and liquidity of the organization | Gives an assessment of the effectiveness of certain indicators of the economic activity of the enterprise. The introduced standards make it possible to identify problem indicators and make management decisions Used to assess the financial performance of enterprises in the same industry |

It is difficult to determine the likelihood of bankruptcy risk and the level of financial reliability |

| Scoring (rating) assessment | Comprehensive assessment of the company's financial condition, solvency and financial reliability. Application of models for assessing the likelihood of bankruptcy, rating models, ballpoint and expert methods | A comprehensive criterion based on a model for assessing the financial condition allows you to determine the likelihood of bankruptcy risk | The final estimate may be distorted due to the peak overestimation of one of the model's indicators |

An example of vertical analysis of the balance sheet for PJSC KAMAZ in Excel

Consider an example of a vertical analysis of the balance sheet for the company KAMAZ PTC. To do this, you need to download the balance from the official website of the company or follow the link →.

We will conduct a vertical analysis of non-current assets, for this it is necessary to assess what part / share is occupied by its constituent parts.

Share of intangible assets (F9) = C9 / $ C $ 18

Share of research and development results(F10) = C10 / $ C $ 18

Share of fixed assets(F13) = C13 / $ C $ 18

Share of profitable investments in material assets(F14) = C14 / $ C $ 18

Share of financial investments(F15) = C15 / $ C $ 18

Share of deferred tax assets(F16) = C16 / $ C $ 18

Share of other non-current assets(F17) = C17 / $ C $ 18

You can see that the sum of all parts will give 100%. The figure below provides an example of conducting a vertical analysis of non-current assets in the balance sheet ⇓.

At the next stage, we can distinguish the maximum and minimum shares in the formation of non-current assets for 2014.

The maximum share in the formation of non-current assets (66.3%) is occupied by fixed assets, the minimum share in the results of research and development (0.4%). To reflect the dynamics of changes in the structure, it is necessary to build a diagram of areas ⇓.

It can be noted that by 2016 there has been a decrease in the share of fixed assets (fixed assets) from 66.3% to 36.1% and an increase in the share of financial investments from 7% to 43%. A decrease in the share of fixed assets may indicate a decrease in the enterprise's investments in production and the development of long-term potential. Fixed assets include: buildings, structures, equipment, vehicles, tools and inventory.

Vertical analysis of the income statement

The versatility of the method allows it to be used to analyze the statement of financial results (form No. 2) and to determine how the share of expenses and incomes changed when generating revenue. For example, let's take the previous financial statements of KAMAZ PTC and reflect the change in revenue indicators for 2015 and 2016. You can see that the revenue is 100%.

Income from subsidies received (E8) = C8 / C7

Cost of sales (E9) = C9 / $ C $ 7

Gross Profit (E10) = C10 / $ C $ 7

All other lines of the income statement are calculated in the same way. The figure below shows an example of using the ⇓ method.

As can be seen from the figure, the cost of goods produced (costs) is higher than the revenue, but the positive revenue is maintained at the expense of income in the form of subsidies.

From 2015 to 2016, there was an increase in the share of gross profit from 4.6% to 9,%, a decrease in profit from sales from 6.2% to 4.4%, a decrease in profit before tax from 4.7% to 1.3%.

conclusions

Vertical analysis is used as a method for analyzing financial indicators from the balance sheet, statement of financial results, and can also be used for the statement of cash flows and for the statement of capital flows. The method is used to assess the dynamics of the structure of assets and liabilities of the balance sheet. To carry out a comprehensive financial analysis, it must be used in conjunction with horizontal and coefficient analysis, as well as assessment by bankruptcy models.

Horizontal analysis means a method of comparing the values of the same indicators over a certain time period. Another name for the method is temporary or dynamic, because the assessment of the change in a certain year compared to the indicator in the previous or baseline is carried out.

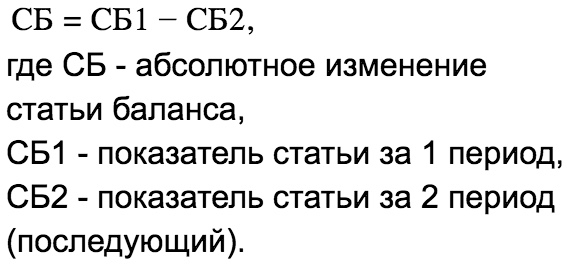

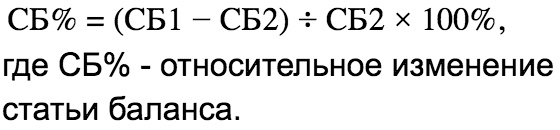

Horizontal analysis involves comparing data from one period with the previous one. As part of the horizontal financial analysis of the balance sheet, a value is compared, for example, of accounts receivable for 2016 with accounts receivable for 2015. The calculation of absolute and relative deviations is an important element of this method. Absolute deviation means the change in the indicator, expressed in rubles or another currency. The relative deviation means the change in the indicator, expressed as a percentage.

In simple words: Horizontal analysis is the comparison of data over time.

Horizontal analysis, like vertical analysis, can also be used when studying the main forms of financial statements of an enterprise: balance sheet, statement of financial results, statement of cash flows. In addition, in the process of analysis, one should compare the increments of indicators from various forms of financial statements, which will make it possible to form additional conclusions and recommendations.

Methodology for horizontal analysis of reporting

The process involves determining the absolute deviation, as well as the relative increase in the indicator. For example, when determining a change in the amount of fixed assets, the formula will look like:

Absolute gain =

the amount of fixed assets in the current year -

The amount of fixed assets in the previous year

Relative gain =

absolute growth

the amount of fixed assets in the previous year

When studying long-term phenomena occurring for three years or more, it is advisable to use deflators to obtain real results of changes in the phenomenon in the process of its development.

When performing an analysis of changes from year to year, observe the following rules:

1. If the item has a value in the base year and is not zero in the next period, the decline is 100%.

2. A meaningful percentage change cannot be calculated if one number is positive and the other is negative.

3. Percentage change cannot be calculated if there is no number in the base period.

Understanding the results of the performed horizontal analysis

The interpretation of the results depends on the phenomenon being investigated. For example, a decrease in the value of fixed assets may be evidence of a decrease in the production potential of the enterprise, i.e. is a negative phenomenon. At the same time, the reduction of unfinished construction projects indicates the introduction of new fixed assets by the enterprise into its activities, i.e. is a positive development. An increase in the amount of equity capital leads to an improvement in financial stability indicators.

Example

When examining financial statements and ratios, it is also important to identify trends, because they are just as important to understanding a company's performance as absolute or relative indicators. Trend analysis provides important information about historical performance and growth and, given a fairly long history of accurate seasonal information, can be of great help as a planning and forecasting tool for managers and analysts.

Table 1 - Horizontal analysis of the balance sheet for a hypothetical company over 5 years, thousand rubles

|

Indicators |

Absolute deviation |

Relative deviation |

|||||

|

Fixed assets |

|||||||

|

Fixed assets |

|||||||

|

Accounts receivable |

|||||||

|

Financial investments |

|||||||

|

Cash and cash equivalents |

|||||||

|

Current assets |

|||||||

Table 1 is a partial balance sheet for a hypothetical company over five periods. The last two columns of the table show changes for period 5 compared to period 1, which is expressed both in absolute currency (in this case, in rubles) and as a percentage. It is worth considering the reasons for the change in order to understand the trends that have formed in the company. In this example, the largest percentage of change is shown by investments, which decreased by 33.3 percent. Nevertheless, a study of the absolute currency amount of changes shows that investments changed only by 2 thousand rubles, and a more significant change was an increase of 12 thousand rubles. accounts receivable.

A horizontal balance sheet analysis highlights the structural changes that have taken place in the business. Past trends are obviously not necessarily an accurate predictor of the future, especially when economic or competitive environmental changes occur. Researching past trends is more valuable when the macroeconomic and competitive environment is relatively stable and when the analyst is considering a stable or mature business. However, even in less stable conditions, historical analysis can serve as a basis for developing forecasts. Understanding past trends is helpful in assessing whether these trends will continue or change direction.

One of the indicators of success for a company is its faster growth compared to the growth rate of the market in which it operates. Companies that grow slowly may not be able to raise capital. On the other hand, companies that grow too quickly may find that their administrative and information management systems cannot keep up with the rate of expansion.

Relationships between forms of financial statements in horizontal analysis

Trend data generated by horizontal analysis can be compared with other elements of financial statements. For example, the asset growth rate for the hypothetical company in Table 1 can be compared to the company's revenue growth over the same time period. If revenues grow faster than assets, then the company increases its efficiency (that is, it generates more revenue for every ruble invested in assets).

As another example, consider the annual percentage change for a hypothetical company:

Revenue + 20%

Net profit + 25%

Operating cash flow -10%

Assets + 30%

Net income is growing faster than revenues, which indicates growing profitability. However, the analyst would have to determine whether the higher growth in net income originated from ordinary activities or from non-core activities. In addition, the 10 percent decline in operating cash flow, despite rising revenues and net income, clearly warrants further investigation as it may indicate problematic earnings quality. Finally, the fact that assets were growing faster than revenues shows a decline in the company's efficiency. The analyst must study the factors behind the increase in assets and the reasons for these changes.

Sources:

Thomas R. Robinson, International financial statement analysis / Wiley, 2008, 188 pp.

Kogdenko V.G., Economic analysis / Textbook. - 2nd ed., Rev. and add. - M .: Unity-Dana, 2011 .-- 399 p.

Buzyrev V.V., Nuzhina I.P. Analysis and diagnostics of financial and economic activities of a construction company / Textbook. - M .: KnoRus, 2016 .-- 332 p.